By Yardi Blog Staff on January 27, 2017 in News

Before the presidential election, the consensus economic forecast was  more of the same slow-growth environment that has prevailed since the Great Recession ended. However, the election of Donald Trump changed expectations for domestic output, prompting interest rates to rise.

more of the same slow-growth environment that has prevailed since the Great Recession ended. However, the election of Donald Trump changed expectations for domestic output, prompting interest rates to rise.

Yardi Matrix vice president Jeff Adler and CBRE Americas head of research Jeanette Rice spoke to these changes and more during the Apartment Markets: The Macro Perspective panel at the National Multifamily Housing Council’s recent Apartment Strategies Outlook Conference.

The panelists discussed what rising interest rates could mean for an interest-rate sensitive asset class such as commercial real estate. Adler asserted that the impact will be determined by how much and how fast rates increase and property performance. A prolonged period of rising rates could diminish property valuations, but at the same time a modest decline in values caused by a one-time bump in rates could be offset with revenue increases.

Although it will take some time before the true impacts can be fully gauged, if interest rates are an indication, then economic productivity and inflation could rise in the coming years. The panelists deliberated upon what happens to cap rates as interest rates and (by extension) property values move higher.

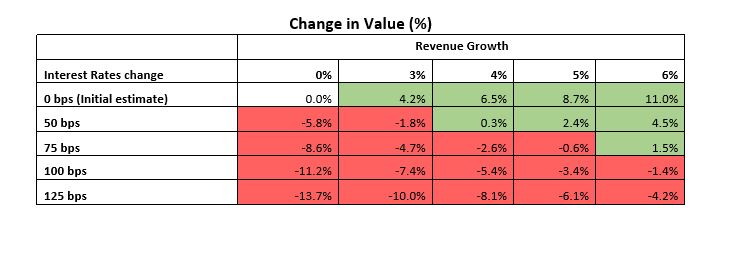

Adler believes that Cap rates are likely to moderately rise and valuations may take a slight hit as interest rates increase, however the key factors will be the pace of rate increases and the concurrent revenue growth.

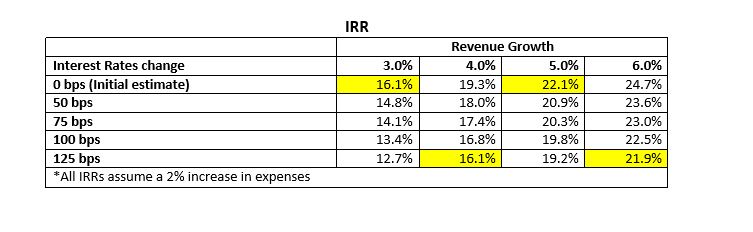

He shared a model that Yardi Matrix® created to predict the impact of both interest rate and revenue increases and determined that mild and steady interest rate increases can be significantly offset by healthy revenue growth, and as a result valuations should remain stable. Looking at an internal rate of return (IRR) calculation, an increase in interest rates marginally affects IRR when revenues are flat, but is offset by continued revenue growth.

Optimistic About Public Policy

Like many of the panels during the strategies conference there was a great deal of uncertainty when discussing how the policies of the new administration will shake out. Panel moderator Mark Obrinsky, Senior Vice President of Research and Chief Economist, noted that the incoming administration brings with it more uncertainty than at any other administration during his career in his career.

Despite this uncertainty, the general sentiment in the multifamily industry is optimistic. Of particular interest for the apartment industry are the reduction of government regulation in the financial sector, tax cuts, and the future of tax provisions such as carried interest and tax-deferred exchanges.

The panel speakers forecast that while the Trump presidency will likely bring expanded economic production, and jobs, which would in turn support the multifamily industry, there are a few potential speed bumps, such as stronger equity values and tighter spreads between cap rates and bond yields.

Both panelists agreed that the recession that seemed to be right around the corner before the election will likely be forestalled for a year or two due to new pro-growth policies. Adler was optimistic that such policies could be well-timed as “monetary policy has gone as far as it can go” in stimulating economic growth.

Supply and Demand

Adler also believes that the multifamily industry is still well positioned to continue its current expansion through 2017 and beyond thanks to favorable demographics. Although there has been a significant increase in supply over the past few years, the demand for housing remains strong, so absorption and occupancy have not suffered.

Factors such as reduced homeownership, downsizing of retiring Baby Boomers, the growing number of Millennials and strong job growth has supported demand for apartments in the long term. In the short term, both Adler and Rice agreed that the days of 4%-5% national rent growth were over, but Adler noted that many individual markets in 2017 will continue to exceed the 5% level.

In the wake of the recession, apartment development declined dramatically, and while developers have ramped up production over the past four years, new supply continues to fall below accumulated household formation. Many Millennials have been living at home or in shared housing due to a tepid job market and housing affordability. With the labor market back to full force and wages finally increasing, new renters are emerging.

With strong demand that supports both continued development as well as rent growth, multifamily values should be able to withstand the recent uptick in interest rates. Given the recent stability in the 10-year Treasury yield, it appears as if the post-election move was more of a one-time adjustment than an ongoing pattern – at least for now.

Adler and Yardi Matrix® expect that increases in cap rates as a result of higher rates will be minimal, and will be made up to some extent by net income gains. Thus, the apartment industry remains well-positioned for 2017, although changes in values are likely to be modest and any gains will likely come from revenue growth rather than appreciation.